Delta is a measurement of how much an option’s price will move based on a $1 move in the underlying asset. For example, if a stock is trading at $50 and the option has a delta of .50, this means that for every $1 move in the stock, the option will move $0.50, and the profit will be 0.5*100= $50.

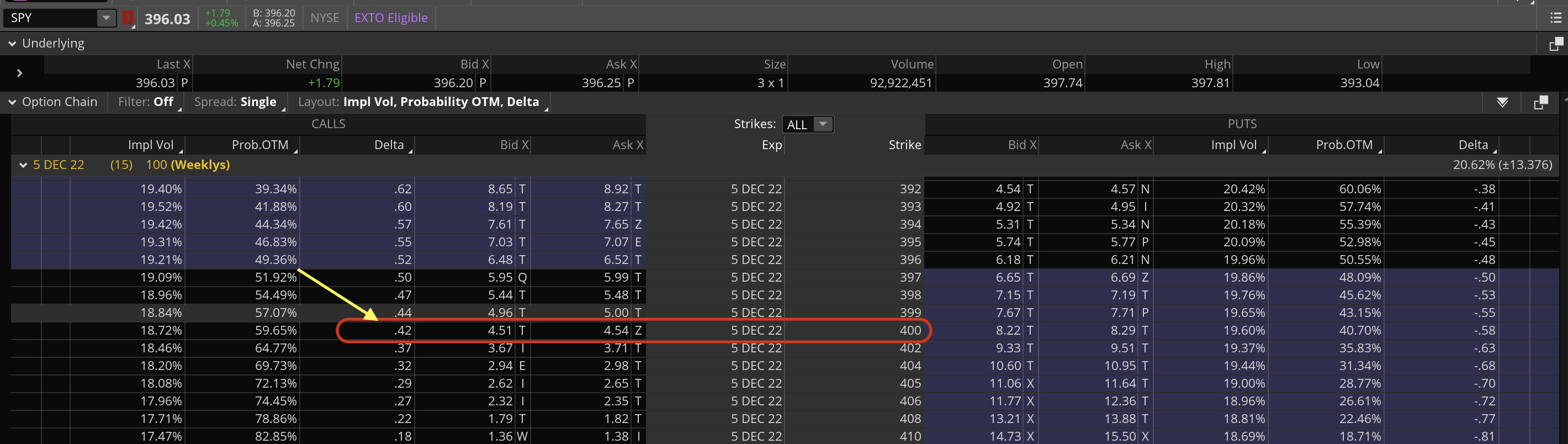

Imagine you bought an OTM call option on SPY with the strike price of $400 and the delta was 0.42 as seen on this options chain. Now, every $1 move up in price will be an additional 0.42 price increase with the option. Call options will have a delta between 0 and 1 while put options will have a delta between 0 and -1. The delta of a call option increases in value as a stock moves up and decreases as the stock moves down. The delta of a put option decreases in value as a stock moves up and increases as the stock moves down.

Because options become more reactive to changes in stock prices as they approach expiration, the delta will increase or decrease at a fast rate. Good news if you are in profit, good news if you are OTM and getting closer to ITM, and bad news if you are OTM and going in the wrong direction.

At the money options will have a delta close to +/- .50. In the money options will have a higher delta meaning they will react faster to the movement in the stock. Look at the delta prices highlighted in the green section (ITM) in the above graphic for examples.

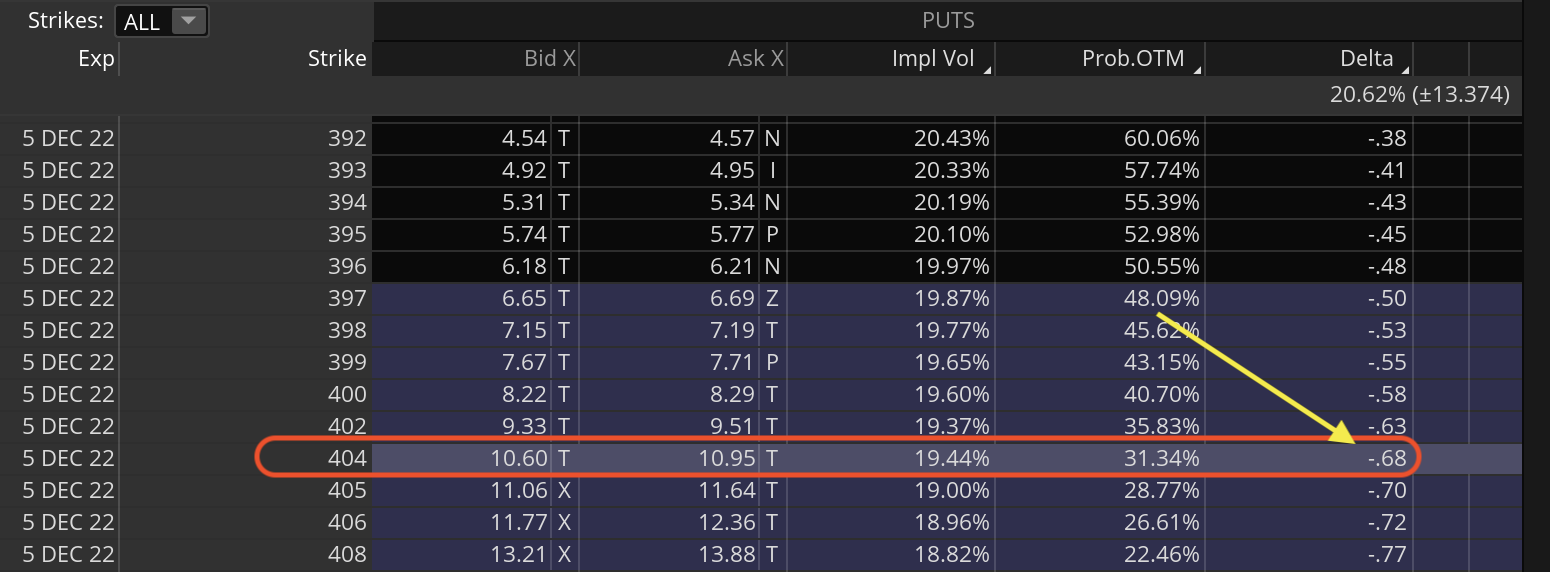

Using a put option example, notice the 404 strike price has a -.68 delta. Every $1.00 move in the underlying stock will move .68 depending on the direction of the underlying instrument.

Delta can also be referred to as the “hedge ratio” as it tells you how many options contracts you need to buy or sell to hedge, or protect, your position in the underlying asset. While delta can be a useful tool for hedging, it is important to remember that it is not a perfect measure of risk. This is because it does not take into account other factors such as time decay and implied volatility. As a result, delta should be used as one part of a broader hedging strategy.

One other feature of the delta is it can give you a rough indication of the probability that an option closes in the money. If you are looking at a put option with a delta of .68, then that option has a 68% chance of being in the money at expiration.